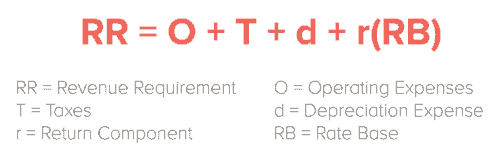

This formula is unknown to the average utility customer, yet utility executives, wonks, and regulators know it by heart. The revenue requirement formula is the basis of the utility rates we pay to charge our smart phone, heat our home, cook our dinner, and water our lawn. Much attention is often paid to the operating expenses and the return component in the equation. By minimizing the operating expenses, rates can be lowered. By increasing the return component, a utility can maximize profit. Often overlooked is the significance of the depreciation expense, the effect it can have on the rate base, and, therefore, the overall return on the utility’s investment.

The purpose of the depreciation expense is to recover the utility’s plant investment incrementally throughout the service life of the asset. A basic principle to ratemaking is to only charge customers for assets that are used to provide them service. Essentially, today’s customers should pay for today’s plant, not tomorrow’s or yesterday’s plant.

Utilities often require millions, sometimes even billions, of dollars of plant investment to bring reliable service to customers. Because this plant will eventually wear out, depreciation expense typically comprises a significant portion of the cost of utility service to a customer. Therefore, the determination of how quickly to recover the investment through depreciation will greatly impact ratepayers and the utility. An excessive depreciation expense will result in higher rates, increased cash flow for the utility, and a reduction in the utility’s return on investment as the rate base is depleted. Conversely, insufficient depreciation expense will result in lower rates, decreased cash flow for the utility, and a greater return on the utility’s investment as the plant remains in rate base longer. Both extremes carry pros and cons for utilities and consumers, and only the development of a reasonable depreciation rate will properly balance the interests.

Though calculating a depreciation rate is simple in concept, the realities of utility operation, the significance of the result, the obscurity of the future, and the need to provide a rationale and supportable defense of the final rate introduces several complexities into the calculation. Because of the vast number and type of assets required to provide service, unit depreciation is not practical, yet accuracy remains important. Estimating a precise service life and final salvage value of an asset, sometimes forty or more years in the future, verges on impossible. Changing utility practices, market, technology, and regulatory forces can also alter even the best projections.

To accommodate these complexities, depreciation models have been developed combining both analysis and professional judgment to produce rational and supportable depreciation rate projections. In order to address the “prediction problem,” a commonly accepted solution is the use of the mortality curves that apply to utility plant. Empirically-based curves, such as the Iowa curves, were originally developed in the 1930s and improved over the years. If the correct curve and average service life is chosen for a specific type of utility asset (e.g. an electric transformer), a reasonable projection of the overall remaining life of the asset account can be determined.

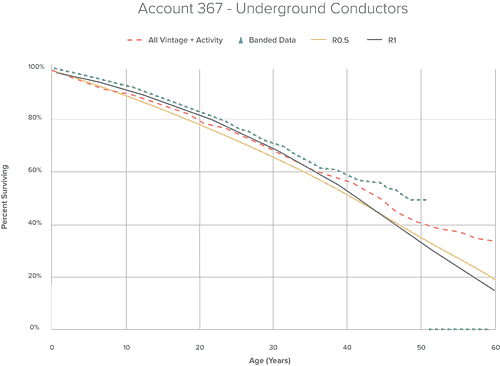

To look forward, we must first look back at the realized utility experience in the continuing property records and use that data. Because of the vast number of utility assets, the years of historical experience and the computational challenges of the calculations, specialized computer models are universally used to crunch the numbers. In certain types of analysis, they also provide graphical tools, such as those shown below, to compare the utility’s asset experience with potential mortality curves so the best life projection can be chosen.

In order to provide this service to our utility clients, Aldrich is in the final stages of development of a data driven depreciation model. The model is designed to adapt to the different quantity and detail of data our clients have available in order to utilize the depreciation system that will produce the most accurate results.

Due to the complexity and volume of the calculations, a reliable computer model is imperative for the preparation of most depreciation studies. In a study, each asset account is carefully analyzed to determine the proper depreciation rate. Then, a well-researched report is prepared to present and defend the selected rates. Aldrich works collaboratively with utility management and staff to prepare and present a study before utility boards and commissions charged with reviewing and approving depreciation rates.

Contact us below for help determining whether a depreciation study would be useful for your utility.

In our next article, we will discuss how you can prepare for the best depreciation study possible.