The new year is a great time to consider taking advantage of the temporary estate, gift, and generation-skipping exemption increases that sunset on December 31, 2025. Planning for the sunset now will help your loved ones avoid unexpected estate and generation-skipping transfer taxes.

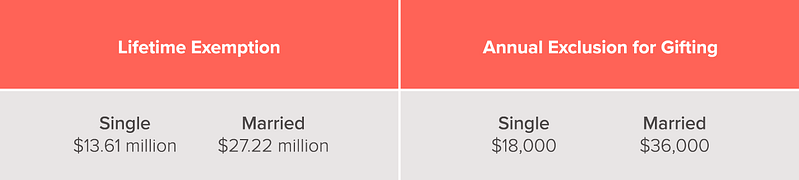

The lifetime exemption and annual exclusions for gifting significantly increased in 2024:

Gifts above the annual exclusion reduce your lifetime amount available to gift or leave to heirs. While this sounds like a large amount, remember that all your assets are included in the total. These assets can be cash, real estate, stocks/bonds, mutual funds, IRAs and other retirement accounts, and potentially life insurance if it is not properly sheltered in an irrevocable trust.

If you have not yet taken advantage of the increased lifetime exemption, the new year is a wonderful time to consider making gifts. Any income-producing property you gift away will transfer this year’s income to other family members, who might be in a lower tax bracket than you.

Increased Lifetime Exemption to Sunset on Jan. 1, 2026

After December 31, 2025, the lifetime exemption equivalent will automatically reduce to about $6.8 million, indexed for inflation. The Tax Cuts and Jobs Act (TCJA), enacted in 2017, raised the exemption equivalent to its current amount.

However, the Act included a sunset provision that automatically reverts the exemption amount to the 2017 figure. Current projections put the inflation-adjusted amount effective for the years after 2025 to be between $6 – $7 million per person. This reduction has the potential to affect many individuals.

“Use It or Lose It”: Take Advantage of the Lifetime Exemption Now

Taxpayers using the increased exemption in effect from 2018 to 2025 will not be adversely affected when the exemption amount reverts to pre-2018 levels. This creates a “use it or lose it” opportunity: if you gift away the additional amount in effect now, the IRS will not claw back any of the excess after December 31, 2025.

Consider this example of the impact of wealth transfer planning: A single individual with an estate valued at $25 million is unsure if they should give away part of their estate now or let their heirs deal with taxes after they die. The following compares how much the individual could save in taxes by gifting the maximum exemption amount in 2024 versus not gifting:

| No Gifting | Gifting Maximum Exemption in 2024 | |

|---|---|---|

| Total Estate Value (after Annual Exclusion) | $25,000,000 | $25,000,000 |

| Gifts in 2024 | ($0) | ($13,610,000) |

| Adjusted Estate Value | $25,000,000 | $11,390,000 |

| Total Estate Value on Death in 2026 | $25,000,000 | $11,390,000 |

| Less Exemption Available/Remaining in 2026 | ($6,800,000) | ($0) |

| Taxable Estate | $18,200,000 | $11,390,000 |

| Estate Tax Due (40%) | $7,280,000 | $4,556,000 |

The tax savings from gifting in 2024 = $2,724,000 or ($7,280,000 – $4,556,000). The tax savings are generated by using the reduction in the exemption equivalent now. The IRS will not recoup the amount used, even though it exceeds post-2025 limits.

A married couple may use a different strategy to achieve maximum estate tax savings: they may elect not to split gifts when filing a gift tax return. If the married couple has an estate valued at $30 million, one spouse can gift the maximum exemption available in 2024, and the other spouse can save their exemption to be used later at their death. Here is an example of the savings possible from this strategy.

| Individual | Spouse | |

|---|---|---|

| Total Estate Value (after Annual Exclusion) | $15,000,000 | $15,000,000 |

| Gifts in 2024 | ($13,610,000) | ($0) |

| Adjusted Estate Value | $1,390,000 | $15,000,000 |

| Exemption Equivalent Remaining After 2025 | $0 | $6,800,000 |

If the couple had elected to split gifts in 2024, each would have applied $6,805,000 of their exemption equivalent to offset the value of the gifts. Thus, neither would have any 2024 exemption equivalent available to use after 2025 when the sunset provision reduces the exemption equivalent down to $6,800,000. This strategy may save the couple or their heirs $2,720,000 in gift and estate tax.

Time Is of the Essence

Even though 2026 is two years away, there are several reasons why we encourage individuals to act now to achieve maximum tax savings. First, economists predict that in the next 25 years, more than $80 trillion will be transferred from parents of baby boomers and boomers themselves to future generations.

Some are calling this the greatest wealth transfer in history, as boomers currently hold half of the nation’s wealth. With estate and gift taxes at 40%, proper planning is essential, or the government may wind up being your largest beneficiary.

The second concern is that there are a small number of advisors who specialize in estate, gift, and trust issues. Those who do specialize in this area are already incredibly busy.

Plan Your Financial Future with Aldrich

This is the time to begin to implement estate and gift planning strategies to ensure your family is protected now and in the future. We have developed several strategies that enable you to use the increased exemption amount, while—in certain cases—allowing you to indirectly benefit from the property gifted. If you’re ready to take advantage of the temporary estate, gift, and generation-skipping exemption, let’s talk.