Originally published on August 1, 2024, this article was updated on September 24, 2024 with the latest information.

On August 1, 2024, the Oregon Secretary of State certified that Initiative Petition 17 (IP–17) had received enough signatures to appear on the state’s General Election Ballot as Measure 118 in November of 2024. Measure 118 would create the Oregon Rebate, a universal basic income program that would provide every state resident with an estimated $1600 annually and would be funded through a new additional minimum tax on corporations in the state.

Potential Impact of Measure 118 on C-Corps and S-Corps

If the Measure is passed into law, Oregon would collect additional revenue of $6.8 billion annually, per the Oregon Department of Administrative Services. This would primarily be used to provide every resident of Oregon, regardless of age, with an annual $1600 rebate check.

The Measure would:

- Impose a new 3% tax on corporate sales in Oregon exceeding $25 million.

- Apply to C-Corps and S-Corps, but not to Partnerships.

- Prevent apportionment and reduction by any credits.

- Base the tax on total sales within the state, not on profits.

- Become effective in 2025.

While the tax would generate significant revenue, it could also potentially raise costs for businesses, potentially impacting prices for consumers.

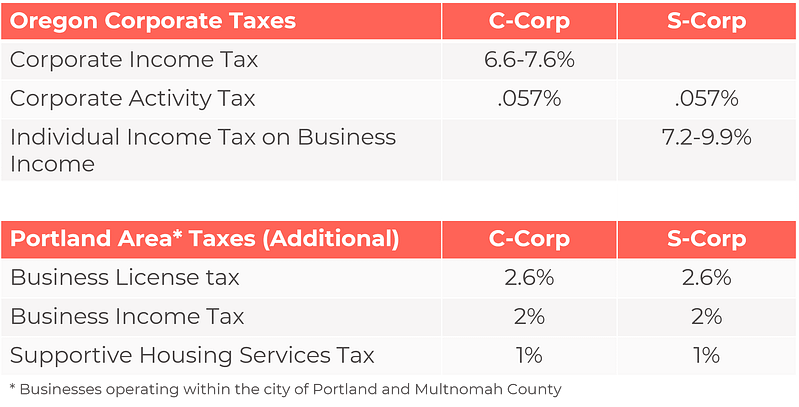

Current Oregon Tax Regime for C-Corps and S-Corps

Oregon’s excise and income tax on corporations is the second largest revenue source for the state, comprising 10.3% of the state’s general fund during 2021-2023. If this Measure becomes a law, it will add to the existing taxes paid by C-Corps and S-Corps in Oregon:

Aldrich Insights

Business owners should consider taking the following steps:

- Monitor updates on the Measure in advance of the November 5, 2024, General Election ballot.

- Ensure you are currently sourcing sales for your state income tax correctly and begin to model how Measure 118 could impact your operations if it becomes law.

- Consider your tax restructuring options, as the initiative does not apply to Partnerships